History has shown us that inflation is the most dangerous economic threat to a country’s well-being and has profound redistributive effects on the social structure and the economy, by altering the rationality of economic calculation, increased inequalities and unfulfilled expectations. Those who have built up savings, with skill and moderation, see how they are being eroded by decreasing purchasing power, and those in debt sometimes breathe a little easier. However, in the long run, inflation thwarts investment plans and slows down development.

Probably the high inflation perpetuated over the years is the strongest brake on prosperity, but also the implacable indication of erroneous public policies, contrary to economic responsibility and financial sustainability.

Returning to high inflation

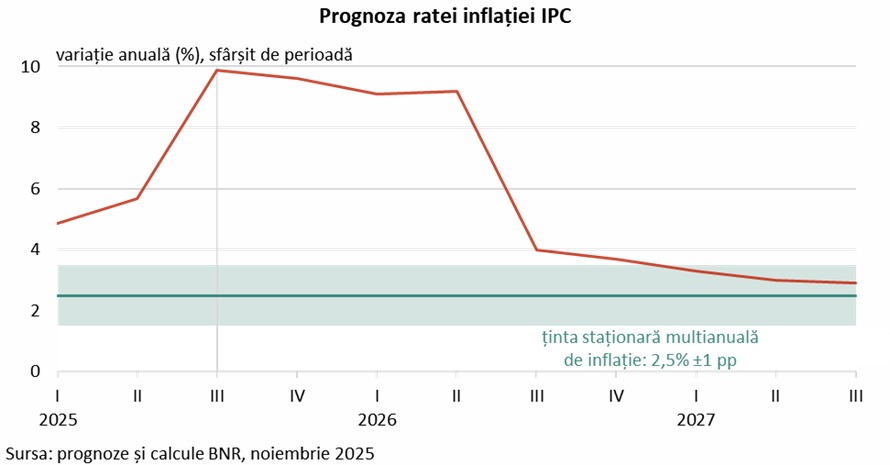

Starting with the middle of 2025, Romania re-entered a stage of high inflation, in fact, the highest inflation in Europe in the current context. Inflation peaked at 9.9% in August and September, then 9.8% in October, and we expect it to remain high in the coming months, but on a downward trajectory.

The recent jump in inflation has mainly administrative springs, not so much monetary, being caused by the increase in electricity prices in July and the increase in indirect taxes starting in August. Of course, these price developments also contain a certain psychological component. Traders have resorted to solutions to protect margins and possibly prevent further worsening of market conditions. And consumers are referring to the new, higher prices for almost all categories of goods, but especially for services, through the considerable and predictable reduction in consumption.

The National Bank of Romania’s (NBR) forecast foreshadowed these peaks in inflation since the summer, with the related risks, especially in the short term. Despite these inflationary pressures, the NBR Board of Directors decided in 2025, in the meetings of August 8, October 8 and, recently, on November 12, to maintain the monetary policy interest rate at 6.5%. At this level, the reference interest rate in 2024 was reduced, from 7% previously, given that inflation had entered, in mid-2024, a slight downward trend, but only temporarily, as we were to observe in just a few months.

A series of questions which are probably justified

Thus, naturally, a series of questions or perhaps perplexities arise, which come in a cascade. Already in the first part of this year, it had become clear that, this autumn, we will witness new peaks in inflation. Then, these questions would say, why did the NBR not act preventively, even in August, or at least in October or November, tighten monetary policy? Isn’t this wait-and-see too long and, more precisely, what does it entail?

Firstly, it must be clearly understood that the current wait-and-see approach to monetary policy is by no means a passivity scenario, but a forward-looking one, of close monitoring of macroeconomic and monetary conditions, and that the instruments at the central bank’s disposal are fully on the “decision table”.

At the same time, understanding and communicating the conditions that must underpin monetary policy decisions are particularly important, especially in the current context, when the contractionary effects of the fiscal adjustment program become a reality.

The GDP contraction of 0.2%, signaled for the third quarter, but especially the economy’s entry into the area of a consistent demand deficit as early as 2025, and much more significant in 2026, when projections show a GDP deviation towards -3.5%, a negative output-gap comparable to the situation of the financial crisis in 2009 and the values of the pandemic years.

Adaptability in an increasingly uncertain world

The fundamental objective of the NBR is price stability, and in order to achieve it, especially today, credibility and adaptability are needed.

The entire planet has been under the impact of a “constellation of shocks” for several years. I subscribe to this characterization from the contemporary debate on the central banking scene. Christine Lagarde, president of the European Central Bank, or Ben Bernanke, former chairman of the Fed, admit the unprecedented intensity and frequency of shocks, especially supply shocks, shocks that have hit in recent years and continue to generate challenges for the entire global economy. Pandemic, armed conflicts, energy crisis, inflation, trade war, all overlap with structural developments of a demographic, technological or climatic nature.

Amid this whirlwind of transformations, monetary policy must remain credible and effective. Monetary policy strategies need to be carefully analyzed and revised, and the tooling needs to be adapted accordingly to ensure price stability.

That 2012 “whatever it takes” by Mario Draghi, the then president of the European Central Bank, a message reiterated by Fed officials with the freezing of the economy during the pandemic crisis, has become a fairly frequently invoked concept, albeit under less dramatic alternatives on the current stage of monetary policy.

Today’s world is increasingly uncertain, and this state of affairs also explains the much more volatile nature of inflation. It is obvious that the frequency and magnitude of shocks are thus much higher, with effects in both directions. For example, analyses show that firms have adapted their strategies, adjusting prices more often and contributing to inflation volatility.

That is why monetary policy needs to consider risks through contextual and forward-looking approaches, not just deterministic correlations. An example is the energy shock generated by the invasion of Ukraine. Risk scenarios based on complex mechanisms have had the ability to project, through the lens of specific models, complicated and comprehensive developments, which standard sensitivity analyses do not adequately capture.

Central bank monetary policy options

The NBR inflation report, as well as the conclusions of the IMF’s country report, both documents published on November 14, highlight a series of arguments and also provide a prospective, medium-term view of the stance of monetary policy. A thorough understanding of the causes of price dynamics and economic activity, as well as of the regional and global framework, these are the elements of the NBR’s information radar, a complex but also adaptable one.

The option of maintaining the monetary policy interest rate, i.e. remaining in the wait-and-see approach, is a perfectly justified reaction that incorporates careful weighing of forecasts and the spectrum of risks. And to understand it, we must, in fact, look at all the monetary policy options available to the members of the NBR Board of Directors.

At the moment, a reduction in the monetary policy interest rate would be, at least from the perspective of short-term risks, practically cut off from everyday financial reality. It is true that we are facing and are facing an even larger demand deficit, but a reduction in the reference interest rate would be contrary to the NBR’s mandate, and would have repercussions not only in terms of prices, but especially in terms of the risk of de-anchoring expectations in the medium term.

Such an undesirable scenario would damage the credibility of the central bank, which would subsequently be forced, in order to bring inflation back within the target range, to take more sudden and restrictive measures for economic activity than would be normal in other circumstances.

Thus, it remains to be analyzed why the increase in the reference interest rate is not justified either. According to projections, in the absence of unpredictable shocks, we expect inflation to mark a steep correction by around 5 percentage points in mid-2026, once the effects of fiscal measures are absorbed into the price system, as shown in the chart below.

It is precisely the temporary nature of the current price advance that explains the current status quo option. Thus, after the 2024 interest rate cut, we avoid placing monetary policy in a carousel of volatility with annual ‘sawtooth’ reactions, i.e. “bottom-up-down”, which would have disrupted the much-needed credibility and predictability.

At the same time, analyzing the decision-making context, we realize that the advance of prices overlaps with the slowdown of the economy. This is after, in 2024, despite fiscal expansionism and record budget slippage, the economy had slowed down, the contraction in investment by 2.5% being doubled by a 4.7% advance in consumption, but largely covered by imports.

Now consumption is mainly affected, suggestive being the 4% contraction in August in retail trade, only partially recovered in September, and by 7.3% in market services, in sync with the -5% decrease in real wage gains. The industry does not show clear signs of recovery either, after marking a 1.9% compression in the third quarter compared to the second quarter. Construction also recorded an annual reduction in August, by -2.1%. And a monetary tightening would have further constrained the financial resources available to firms and consumers.

Principles in price formation

In order to formalize this dynamic of monetary influences, let us recall the equation that describes simply and expressively the quantitative theory of money, M v = P Y, in other words the balance between, on the one hand, the money supply and the velocity (turnover) of money, and on the other hand, the level of prices and the volume of production, in a causal register that must be read only from left to right, that is, from the money supply to prices.

In this correlative key we can invoke the famous conclusion of the empirical research of the monetarist Milton Friedman, winner of the Nobel Prize in economics in 1976, according to which “inflation is always and everywhere a monetary phenomenon, that is, there can be no inflation without the increase of the money supply”. In the long run, we might add.

For example, throughout 2024, the increase in the money supply in Romania occurred mainly through the expansion of government credit, by 27%, a dynamic three times higher than that of private credit. Seen in structure, household consumer credit increased in 2024 by 17.4%, contributing to the persistence of core inflation above estimates. Data for the first three quarters of 2025 show a moderation of private lending, including consumer credit, to 12.3%. And in real terms, non-government credit even recorded a compression, by -2.2%.

Over time, it is true, many economists have criticized some elaborations of monetarist theory, but they have also developed related reasoning, and we mention here Robert Lucas Jr., Friedman’s student at the University of Chicago. Thanks to him, we are now aware of the role of expectations, but also of the limitations of the technical analysis tools in the event of major changes in economic policies.

However, contemporary monetary policy practice remains based on certain key principles of monetarist theory, namely price stability as a fundamental objective, preference for rules versus discretion, as well as medium-term orientation, given the transmission lag. Lag can vary from one economy to another and stems from the complexity of the channels through which the key interest rate passes, through markets and expectations, into the real economy and inflation.

Returning to the arguments of the NBR decisions, the most important aspect to remember is the fact that the current price jump is only temporary, the main cause not being a monetary one now, as I mentioned. This temporary nature of the price increase is explained by the transitory nature of the direct effects of the administrative-fiscal measures acting on price dynamics for a period of several quarters.

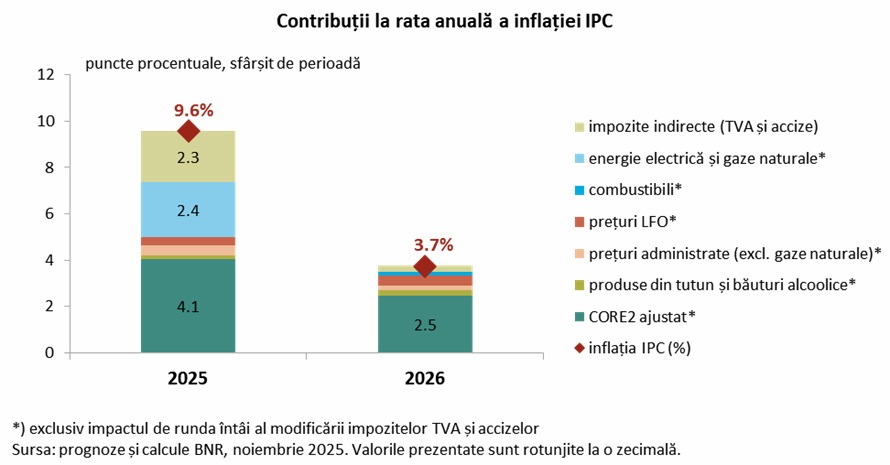

As the figure below highlights, expert estimates indicate that almost half of the current inflation is attributed to the change in VAT rates and excise duties and, respectively, to the increase in energy prices. However, from the middle of next year, the inflationary surge generated by these causes will come out of the calculation of annual inflation.

As such, we expect prices to slow down significantly in about two quarters, under the pressure of strongly suppressed consumer demand, towards annual inflation of 3.7% at the end of 2026, well below what we are currently seeing.

From a monetary policy perspective, it can be considered problematic that the current price jump nevertheless overlaps with still high core inflation, whose monetary incentives cannot be neglected. Moreover, the reactivation of inflation in the last months of 2024 and the persistence of inflationary pressures in the first part of 2025 are developments that also draw attention to the implications that are manifested in the monetary policy sphere.

The price stability objective, seen from the perspective of the return of inflation to the target range, can be effectively achieved through a gradual, precise and consistent implementation of the monetary policy strategy.

Predictability and consistency of monetary policy

Monetary policy works like a heavy ship, with the clear objective of positioning itself on a certain corridor. When a change of direction of navigation is decided and the ship’s rudder is rotated accordingly, only after a while is it seen how the ship turns towards the set course. And the rougher the waters, the more difficult the steering transmission is to achieve. Therefore, in order to correctly place the ship in position, without the need for urgent and costly corrections later, decisions regarding the initiation, intensity and duration of the turn are essential.

All the more so in these complicated times, with rough or troubled waters, in the key of the above example, with challenges on multiple levels, monetary policy must be predictable and consistent. After the wait-and-see approach, the transition to the next stage, of monetary policy interest rate cuts, will only be synchronized with the determined and sustained decrease in inflation.

Let us recall that in July and August 2024, the NBR decided to reduce the monetary policy interest rate by 25 basis points each. Also taking into account the lag in the transmission of monetary policy, the momentum at that time largely overlapped with the inflationary pressures generated by exuberant fiscal policy, in the context of the 2024 election year marked by unprecedented budgetary excesses, if only if we refer to the repeated increases in pensions and wages.

As proof, core inflation stubbornly remained visible, at over 5%, consistently positioned above estimates at the end of 2024. In fact, core inflation showed no signs of declining even in the first part of 2025, before fiscal measures led to the recent jump in prices, the intensity of which raised the headline inflation rate to levels close to 2 digits.

Under these conditions, the transition to a new phase of monetary policy must be prepared carefully and patiently, especially given that core inflation also rose in August to around 8% and remained close to this level in September and October. Moreover, core inflation, with monetary incentives superimposed on the rigidity of competitive mechanisms, could be more persistent than expected, under the action of possible wage increases decoupled from productivity.

At the same time, in the context of the risks that may foreshadow a possible technical recession, lag in monetary transmission must be taken into account, so the timing of decisions becomes crucial. In fact, recent studies on the practice of monetary policy after the financial crisis highlight the importance of temporizing the decisions of the major central banks in order to minimize, in the fight against inflation, the losses in terms of economic output.

Let’s not forget the fact that, through the dynamics of imports, inflation in Romania also mirrors the exchange rate situation. The NBR has the ability to mitigate exchange rate volatility and had to do so. At present, however, the general conditions are compatible with a certain stability of the exchange rate, which remains an anchor of confidence in the economic system. In the medium term, greater flexibility of the leu would also increase the resilience of the economy to shocks, but the condition for a gradual transition is, however, related to the adequate explanation of financial factors and the economic situation.

Regaining financial sustainability

The implementation of the fiscal-budgetary adjustment is closely followed, not only internally, but especially on the European scene. So now we need to prioritize financial sustainability. Any slippage in the rating would have a negative impact on the development prospects. It is gratifying to see, lately, a series of positive assessments of the fiscal-budgetary adjustment measures, materialized in the reduction of the state’s long-term financing costs, below the level of 7%.

Structural reforms are key to regaining financial sustainability and credibility. And for this, it is necessary to synchronize and prioritize economic policies correctly so as to deliver the correction of the budget deficit. Romania’s commitments, as an EU member state, must be treated seriously, as well as the objective of joining the OECD, a new anchor for the country’s economic potential. In fact, as highlighted at the recent meeting of the IMF and the World Bank in Washington, through the voice of Director Kristalina Georgieva, strengthening public finances and reviving sustainable economic growth are global priorities.

Indeed, inflation spikes are serious challenges to monetary policy and the resilience of the economy. But if inflation is temporarily volatile, it does not mean that the benchmark interest rate should become the same, by simplistically activating this correlation.

At present, a scenario of an increase in the monetary policy interest rate would be conceptually similar in reaction to last summer’s tapering, when disinflation had not become sufficiently clear and sustainable, given the broad-based expectations of corrective action through the increase in indirect taxes.

That is why we must stay as far away as possible from the logic of cyclical reactions, which can later be invalidated by developments in terms of prices and the economy in general. The not at all simple task of monetary policy is to avoid in any context, as far as possible, putting “gas on the fire” or “salt on the wound” in relation to the cyclical position of the economy.

In the coming period, the persistence of the monetary policy stance and the transition to the next cycle of interest rate interventions must be carefully calibrated. That is why it is essential that monetary policy decisions favor a sustainable return of inflation to the target range. In this direction are also part of the steps we are taking, to carefully communicate decisions in relation to the relevant economic developments and the most viable projections that we can make within the NBR.

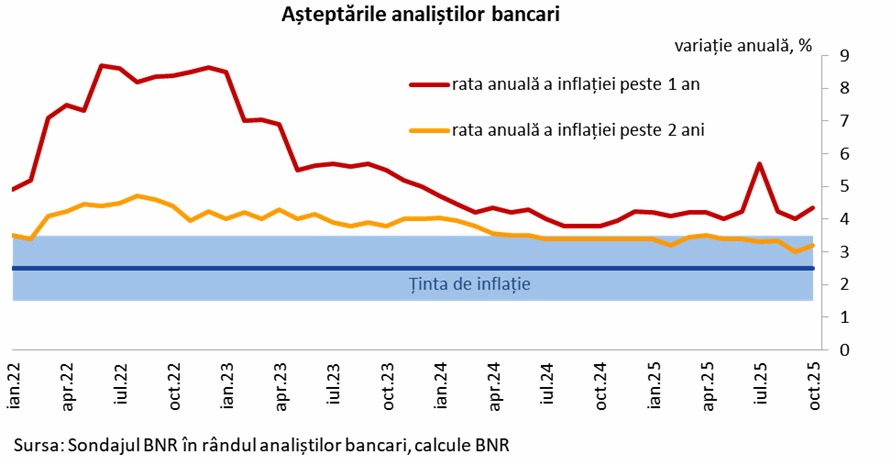

Inflation is now high and certain risk factors still persist. However, given the transmission gap in monetary policy, there is virtually no justification for a change in the benchmark interest rate in relation to the current deviations, which will soon be exceeded. This outlook is also reinforced by the reasonable anchoring of inflation expectations in the medium term, as can also be seen from the expectations of banking analysts.

Currently, it is essential for Romania to consistently return to financial sustainability, and the current efforts to consolidate public finances must be supported politically and societally, with balance and wisdom, in order to regain the necessary economic credibility. This is, incidentally, the key ingredient of financial stability.

Romania’s persistent inflation, a dilemma for the National Bank