: Lia Savonea trebuie exclusă din magistratură")

With or without a lasting truce, the war in the Middle East is fueling severe uncertainty, driving up inflation in tandem with slowing economic activity. In the short term, the impact on inflation results directly from the increase in fuel prices. However, the long-term effects are much more difficult to project, as they depend both on the duration and intensity of the conflict and how they are reflected in consumer prices.

The current energy situation is exactly the kind of external shock, devoid of monetary causes, that central banks should theoretically “overlook”, at least for now. However, both the development of risk scenarios associated with forecasts and the effective communication of monetary policy approaches are particularly important.

The current situation is, in fact, complicated, given the fragile fiscal situation and recent political instability, factors that also leave their mark on monetary policy.

Immediate implications and revision of forecast scenarios

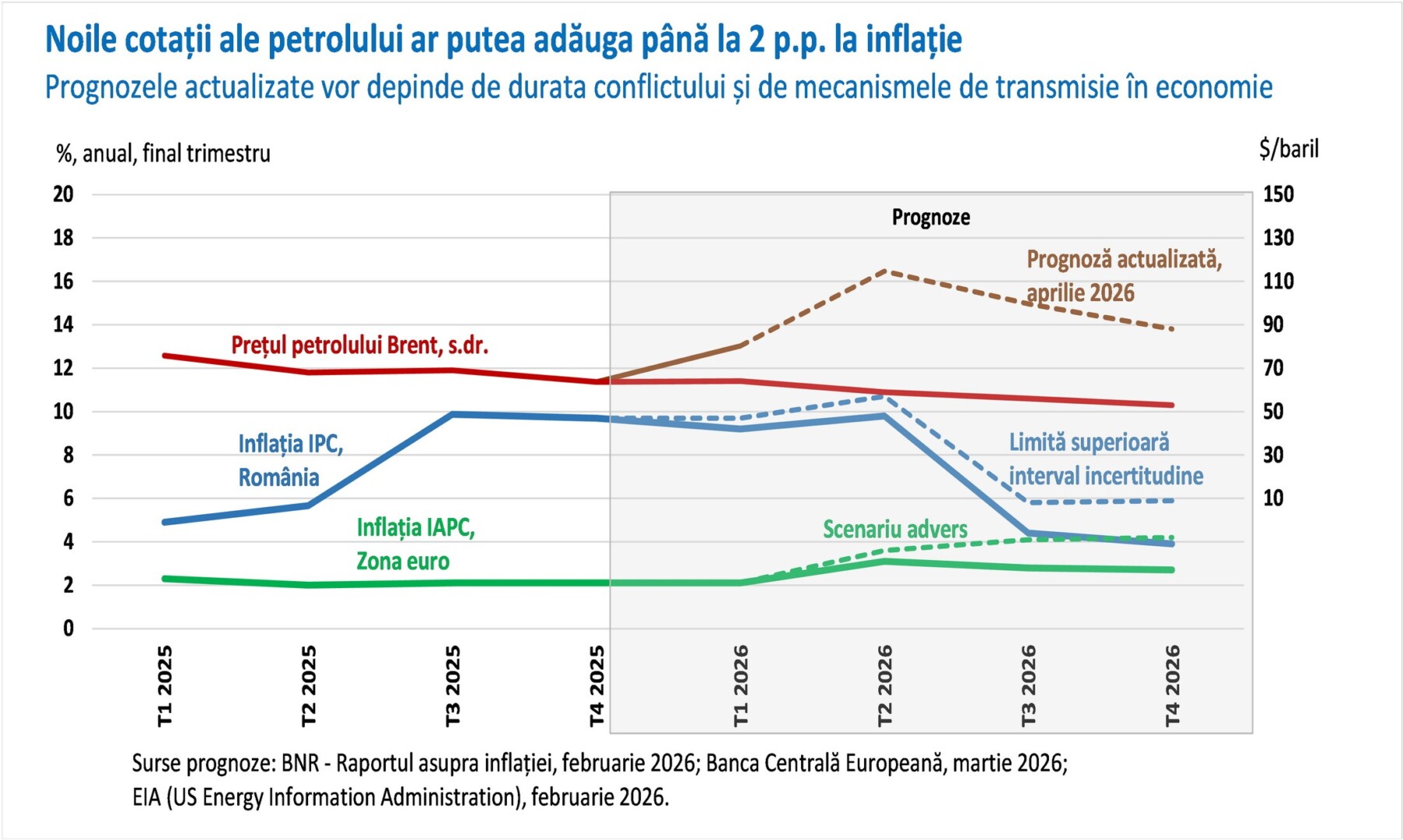

The price of oil (Brent) in March – $103/barrel was, on average, about 50% above that of the first two months of the year, and in April it increased to about $115/barrel. In the EIA’s forecast for the second quarter, the price of oil appears above $110/barrel.

Consumer prices feel this shock almost instantly and even anticipated it, especially in the fuel channel. However, the most exposed to a longer-term acceleration are production costs, which will continue to put pressure on consumer prices.

According to the chart above, for the end of this year we can estimate increases of 1.5 – 2 percentage points – Hormuz inflation – above the projected inflation trajectories in the absence of the Gulf shock, but the spectrum of risks is actually much deeper.

The war is already causing major disruptions in supply chains, with European manufacturers reporting the largest extension of delivery times in nearly four years. Short-term indicators capture this deterioration: for example, the Purchasing Managers (PMI) on economic activity in the euro area fell in March to 50.7 and in April to 48.6, below the threshold that separates the prospects of growth from that of an economic contraction.

In Romania, despite the deficient phase of demand in the economy, the increase in energy prices caused inflation to rise above expectations in March, to almost 10%. The main cause was the increase in fuel prices by about 13%, and April will bring a new boost in inflation, to over 10%. Inflation is affecting already compressed consumption: as early as February, retail sales were down by 6.8% compared to last year.

The prospects for the coming months are not encouraging, with oil tanker traffic in the Persian Gulf still being obstructed. If the tension continues, high energy prices could, through second-round effects, force the persistence of “Hormuz inflation” for several quarters. A counterweight is however given by the capping, for household consumers, of the purchase price of gas from domestic production.

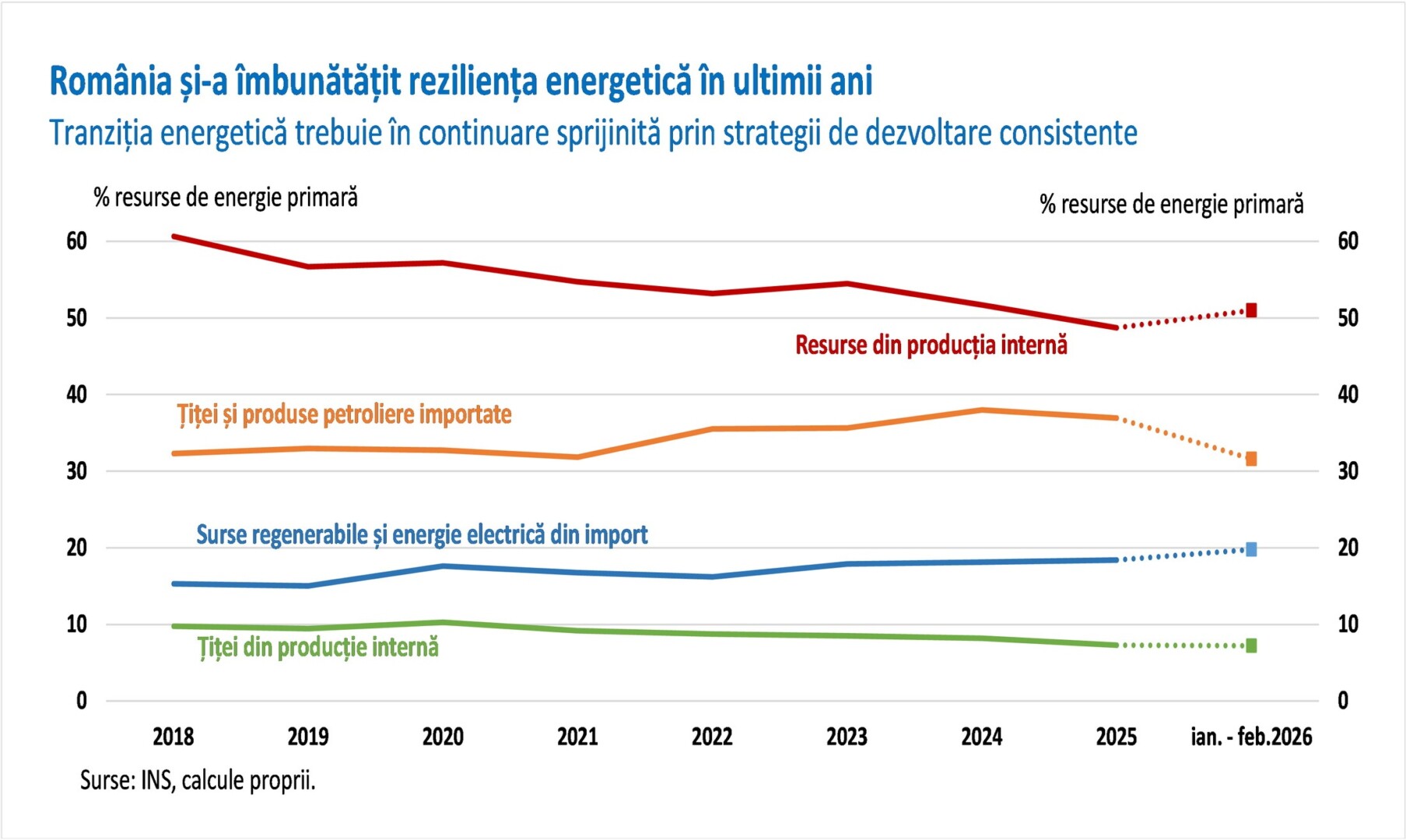

Romania’s energy dependence is lower compared to most European states. But the current situation still underscores the need to further reduce dependence on fossil fuels. As can be seen in the diagram above, imported oil accounts for only a third of primary energy resources.

How (and if) central banks respond to Hormuz inflation

The type of shock, the economic situation and the balance of risks determined, at the meeting of the NBR Board of Directors in April, a wait-and-see reaction, which was expected. But the NBR’s response must be seen in a broader context.

The war has inflamed the price of crude oil, generating a rapid rise in global inflation and fueling risks. The textbook reaction of central banks was to avoid changing the parameters of monetary policy. This attitude may change if the amplification of the energy shock and the inflammation of inflationary expectations become evident.

The succession of crises in recent years has induced a certain capacity for structural change in inflationary expectations. And now, when the globalized trading system is fractured by tariff wars, the situation becomes even more tense. Although the immediate response of the central banks (ECB, Fed, Bank of England) was one of preserving monetary conditions, following the theoretical custom, it is possible that the next steps will move away from this framework. There seems to be some consensus on the need for concrete action, if the Strait of Hormuz does not become generally accessible again soon.

Inflationary risks are significant, at least in the short term, and additional long-term pressures stem from the fragmentation of supply chains, limiting the supply of raw materials. An easing of tension would, however, result from alternative transit channels, which would allow over-produced countries to increase exports.

At the same time as inflationary pressures, negative influences on the growth prospects are looming. The conflict in the Gulf is a slowing factor for the global economy, at least 0.3 percentage points lower than the average of the last two years (3.4%), according to IMF estimates.

At the regional level, the new energy shock overlaps with the uncertainties generated by the conflict in Ukraine. For example, for Romania, the forecasts of the World Bank and the The IMF is significantly revised downwards (by 0.7 percentage points) to 0.5% and 0.7% respectively. In this context, the NBR remained in the cautious area of forecasts, including taking into account the persistent effects of the “technical recession” at the end of last year.

The messages and actions of central banks are calibrated in the format of scenarios that depend on the persistence of geopolitical tensions in the Gulf. The highly inflationary scenarios signal the need to raise interest rates, a prospect that would further slow down economic activity. Messages built around a firm commitment to the inflation target contribute to a better anchoring of inflationary expectations, without the central bank having to act quickly on monetary levers.

An intervention now, by tightening monetary conditions, could prove premature from the perspective of synchronizing the effects in the economy, in the event that the conflict ends relatively soon, and oil tankers resume their route through the Strait of Hormuz.

The rest of the article can be read here.

Powering the future: the race for AI is shifting to the energy sector